After the long holiday, urea prices in various parts of the country have been shown to be exhausted, and the long-awaited price reduction is about to begin. For the fall process expected in the current round, most dealers are waiting and watching, and more are still considering the necessity of procurement. After all, the off-season reserves have a long period of time, and businesses need to take more risks. Not to mention that the profits of the domestic agricultural distribution industry have improved significantly this year compared to previous years, so that this part of the profit-making dealers is not willing to take risks. Therefore, even if the urea companies hit a price reduction promotion card, businesses will be more cautious.

First of all, the annual output of urea. Judging from the overall supply and demand in the first three quarters of this year and the start of the nationwide urea business, it can be sure that the excess production. The annual operating rate of about 80% is matched with the total output capacity of 73 million tons of urea. Without accidents, the total output of urea in the country is expected to reach 58 million tons, which is a market demand of only 52 million tons. It is hard to deal with.

(Source: China Business Network)

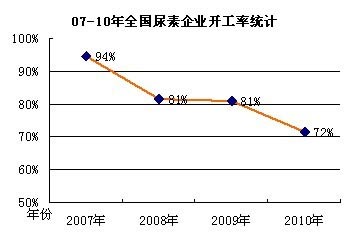

The picture above shows the annual average operating rate of urea enterprises in the country. It can be seen that since 2007, due to the emergence of new urea companies that have been put into operation in China, the situation of overcapacity has become more serious. As can be seen from Table 1, from 2007 to 2010, the total domestic urea production capacity has rapidly increased from 54 million tons to 72.69 million tons. This has further triggered a "price war" among companies, and pure price reduction promotions have also taken away profits. Lead to more urea manufacturers limit production insured prices. Therefore, we can see that in the two years of 2008 and 2009, the urea industry can only maintain an 81% production level to regulate market supply and demand. Even so, annual production is difficult to digest.

Table 1: Apparent Consumption of Urea Statistics Unit: 10,000 tons annual capacity agricultural (physical) industrial (physical) exports (physical) apparent consumption 2010 7269 3781 700 703 5184

2009 6758 4804 500 338 5642

2008 6300 4414 800 436 5650

2007 5400 4015 700 525 5240

(Source: China Business Network)

Take 2010 as an example: Due to the limitation of energy conservation and emission reduction, the total urea output in the year was 52 million tons, a year-on-year reduction of 3 million tons, and the operating rate was calculated to 72%. At the same time, 7 million tons of urea were consumed in exports and in industry. Under such circumstances, the domestic market can still reach a balance between supply and demand. This just allows us to more clearly see the apparent consumption. Then, the expected output of 58 million tons this year will add to the sharp drop in exports. According to preliminary estimates, at least 10 million tons of surplus production will be produced during the year.

Second, there is no sign of starting up. Although the tender for urea light storage in 2011 ended at the end of September, the downstream distributors still lacked the enthusiasm for purchasing and the sales of enterprises were not satisfactory. There are two reasons. First, the merchants have referenced the bottom line price of 1,850 yuan/ton during the 2010 fade-out period; on the other hand, they also considered the demand for the spring plowing in 2012. The above-mentioned excess output of 10 million tons will be directly passed on to the market next year. As a result, business sales pressure will further increase. The price reduction promotion may be the only means of sales for the manufacturer, so in the eyes of the light-storage trader, the ex-factory price of urea may fall below 2,000 yuan/ton.

To sum up, there will definitely be a game process in which manufacturers will focus on prices in the fourth quarter. According to the current market inventory is low and the objective factors of compound fertilizer companies waiting to purchase raw materials. The price of urea temporarily does not have the conditions for a sharp drop. At least there is also the procurement of compound fertilizer companies and some large companies as support. According to the results of India's October 5 bid, once the domestic urea price dropped to 2,100 yuan/ton, it would have met the CIF of 522 US dollars/ton, and exports will also have improved. Therefore, the recent price reduction is likely to fluctuate for a week at the position of 2,100 yuan, but this part of the demand is difficult to achieve sustained price stability. Afterwards, it will start to drastically reduce prices with the standard of light savings.

First of all, the annual output of urea. Judging from the overall supply and demand in the first three quarters of this year and the start of the nationwide urea business, it can be sure that the excess production. The annual operating rate of about 80% is matched with the total output capacity of 73 million tons of urea. Without accidents, the total output of urea in the country is expected to reach 58 million tons, which is a market demand of only 52 million tons. It is hard to deal with.

Statistics on Utilization Rate of Urea Enterprises in China in 2007-10

(Source: China Business Network)

The picture above shows the annual average operating rate of urea enterprises in the country. It can be seen that since 2007, due to the emergence of new urea companies that have been put into operation in China, the situation of overcapacity has become more serious. As can be seen from Table 1, from 2007 to 2010, the total domestic urea production capacity has rapidly increased from 54 million tons to 72.69 million tons. This has further triggered a "price war" among companies, and pure price reduction promotions have also taken away profits. Lead to more urea manufacturers limit production insured prices. Therefore, we can see that in the two years of 2008 and 2009, the urea industry can only maintain an 81% production level to regulate market supply and demand. Even so, annual production is difficult to digest.

Table 1: Apparent Consumption of Urea Statistics Unit: 10,000 tons annual capacity agricultural (physical) industrial (physical) exports (physical) apparent consumption 2010 7269 3781 700 703 5184

2009 6758 4804 500 338 5642

2008 6300 4414 800 436 5650

2007 5400 4015 700 525 5240

(Source: China Business Network)

Take 2010 as an example: Due to the limitation of energy conservation and emission reduction, the total urea output in the year was 52 million tons, a year-on-year reduction of 3 million tons, and the operating rate was calculated to 72%. At the same time, 7 million tons of urea were consumed in exports and in industry. Under such circumstances, the domestic market can still reach a balance between supply and demand. This just allows us to more clearly see the apparent consumption. Then, the expected output of 58 million tons this year will add to the sharp drop in exports. According to preliminary estimates, at least 10 million tons of surplus production will be produced during the year.

Second, there is no sign of starting up. Although the tender for urea light storage in 2011 ended at the end of September, the downstream distributors still lacked the enthusiasm for purchasing and the sales of enterprises were not satisfactory. There are two reasons. First, the merchants have referenced the bottom line price of 1,850 yuan/ton during the 2010 fade-out period; on the other hand, they also considered the demand for the spring plowing in 2012. The above-mentioned excess output of 10 million tons will be directly passed on to the market next year. As a result, business sales pressure will further increase. The price reduction promotion may be the only means of sales for the manufacturer, so in the eyes of the light-storage trader, the ex-factory price of urea may fall below 2,000 yuan/ton.

To sum up, there will definitely be a game process in which manufacturers will focus on prices in the fourth quarter. According to the current market inventory is low and the objective factors of compound fertilizer companies waiting to purchase raw materials. The price of urea temporarily does not have the conditions for a sharp drop. At least there is also the procurement of compound fertilizer companies and some large companies as support. According to the results of India's October 5 bid, once the domestic urea price dropped to 2,100 yuan/ton, it would have met the CIF of 522 US dollars/ton, and exports will also have improved. Therefore, the recent price reduction is likely to fluctuate for a week at the position of 2,100 yuan, but this part of the demand is difficult to achieve sustained price stability. Afterwards, it will start to drastically reduce prices with the standard of light savings.

Belyn Hardware Factory , http://www.xy-hardware.com